Authorization proves that a payment can move. It does not prove that an agent bought the right thing.

That distinction becomes load-bearing the moment users delegate spend to agents. A platform can issue a card, set a limit, approve a merchant, and authorize the charge. The transaction can still be wrong: wrong SaaS tier, wrong vendor, wrong renewal term, wrong travel date, wrong contract condition.

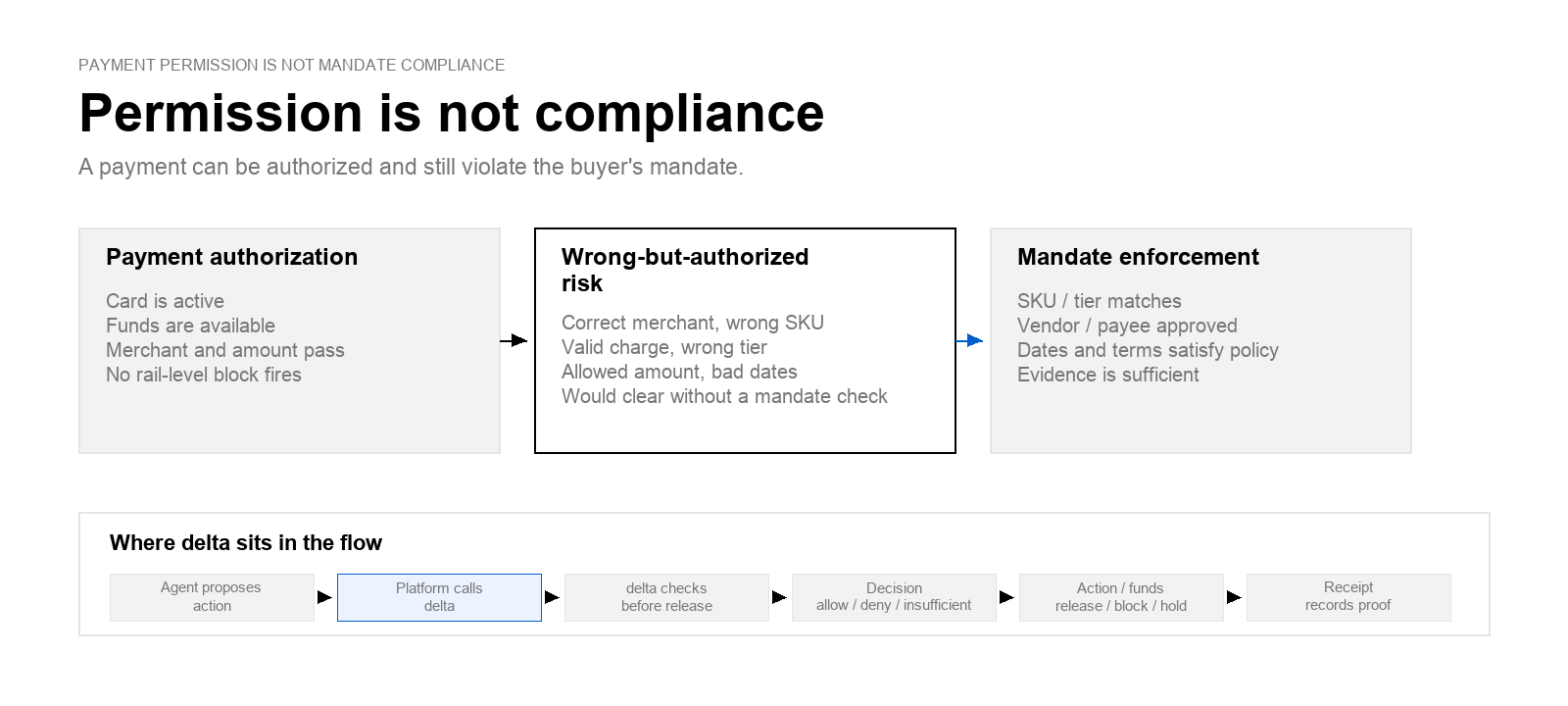

For agentic payments to move beyond low-value tasks, platforms need a second check before funds are released: did the agent's proposed action satisfy the user's mandate?

Authorization Answers The Rail Question

Payment authorization is necessary. It answers whether a transaction is valid from the rail's perspective: card active, funds available, merchant reachable, amount within allowed limits, no hard block triggered.

That is the right question for moving money. It is not the right question for verifying delegated intent.

The rail generally does not know which SKU the agent selected, which contract tier was approved, whether the vendor matches the approved-vendor list, whether the hotel date matches the flight arrival, or whether a renewal term changed from monthly to annual. Those details live in the purchase context, not in the authorization message.

The result is a gap that traditional spend controls do not close. A payment can be permitted and still violate the buyer's mandate.

The Failure Mode Is Not Fraud. It Is Wrong-But-Authorized Spend.

Consider a SaaS renewal. A user authorizes an agent to renew a project-management subscription at the current tier. The vendor checkout defaults to a higher tier. The merchant is correct. The amount is plausible. The transaction is under the platform's limit. Authorization succeeds.

From the rail's perspective, nothing failed.

From the buyer's perspective, the agent violated the mandate.

The same pattern appears in travel and procurement. A travel agent can book a hotel one night after the flight arrives. A procurement agent can pay an invoice with a substituted payee. A purchasing agent can select the correct vendor and the wrong item variant.

These are not edge cases. They are the normal failure modes of agents operating across multi-step, multi-merchant workflows where the user's intent spans more than one payment field.

Spend Controls Limit Magnitude. They Do Not Prove Mandate and Policy Satisfaction.

Spend caps, merchant locks, category controls, and approval thresholds are useful. They reduce blast radius. They make some kinds of misuse harder.

They do not answer the question that matters in delegated purchasing: what was actually bought, and did it satisfy the user’s mandate?

A $500 limit does not distinguish between a $480 renewal at the approved tier and a $480 renewal at the wrong tier. A merchant lock does not verify the SKU. An approval threshold does not catch a travel bundle with mismatched dates. A post-authorization alert can notify the user after the fact, but it cannot prevent funds from moving.

Agentic payments need a pre-execution enforcement step, not only post-hoc review.

Where delta Fits

delta sits between the agent's proposed action and payment release.

The flow is simple:

- The user authorizes a mandate: vendor, amount, tier, dates, contract terms, budget, or any other constraint.

- The agent proposes an action.

- delta evaluates the proposed action against the mandate before funds move.

- delta returns allow, deny, or insufficient evidence.

- If the action is allowed, payment can proceed and a mandate execution receipt is generated.

- If the action is denied or evidence is insufficient, payment does not release and the platform can route the exception.

The mandate execution receipt records what the user authorized, what the agent proposed, what evidence was checked, what decision was returned, and what guarantee boundary applies.

That receipt matters because it gives product, risk, support, finance, procurement, legal, and engineering the same record. No one has to reconstruct the enforcement step from payment logs, agent logs, support tickets, and procurement records after something goes wrong.

The mandate guarantee makes the boundary commercially usable

Evidence alone is valuable. But users also want to know what happens if the enforcement layer was wrong.

The mandate guarantee is delta's bounded commitment around its own enforcement decision. If delta returns allow on an in-scope action that should have been denied given the policy and evidence available at decision time, delta makes the user whole.

That boundary is intentionally narrow. It does not cover every bad purchase, merchant fulfillment issue, agent misrepresentation, or ambiguous policy. It covers delta's own in-scope enforcement failure. The mandate execution receipt is the artifact that makes that boundary auditable.

What This Changes For Platforms

For platforms, the implication is practical. Agentic spend products do not only need better authorization controls. They need a way to prove delegated intent was enforced before payment.

The first workflows are narrow: SaaS renewals at approved tiers, vendor payments against approved payees, travel bookings with date constraints, contractor payments tied to milestone rules. In each case, the platform can test one policy class, one transaction flow, and one success metric: fewer manual reviews, cleaner exception routing, higher delegated limits, or faster dispute resolution.

Authorization will always be necessary. It will never be sufficient. The missing layer is mandate enforcement before funds move, backed by a receipt that shows what happened and a guarantee that makes the downside legible.